|

|

|

|

|

|

|

Ph 0800 828 222

|

|

|

|

|

|

|

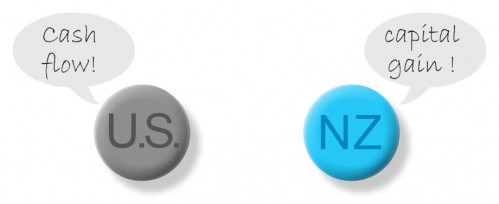

Invest in US or NZ property market?

A brief overview of the pros and cons of both the NZ and US property markets.

Pros

For Investors who must have good cash-flow and earn income from their investment, the US market is almost unbeatable. Like for like (in cash-flow terms), US properities will always out perform NZ properties. This means show us an NZ property returning a net 1-2% and we'll show you a comparable US property returning 10%, show us NZ 10% and we'll show you 20% or 30% or 40% etc.

Relatively low risk in terms of capital cost. For example, with USD $200K, we could buy 3 or more, three-bedroom homes on 1/4 acre sections in a major US city of a million plus people, whereas with the same money in NZ, in a comparable city, we could only by the letterbox and driveway for one house.

The US market has hit a 30yr low in terms of their property prices and the NZ dollar is at a 30yr high enabling us, at this time, to buy a lot more property for our money.

Cons

Whilst the US is now widely expected to experience steady capital growth in the years ahead, we suggest Investors looking for the really big capital gains from their property investments should stick with NZ. Certainly unless the NZ government and/or RBNZ intervenes with some radical 'market-cooling' strategies, the NZ property bubble should continue to out perform most other international markets in terms of capital growth.

Exchange rate adds an element of risk that is not present when investing in the local NZ property market. In particular, Investors should carefully assess the following two situations carefully before Investing in any international property:

i) If the New Zealand dollar strengthens against the US dollar, then the Investor will realise a loss when and if they bring the original capital investment back to New Zealand.

ii) Investors who wish to borrow and buy US property should borrow from US loan facilities, so that a shift in exchange rate does not impact on debt servicing costs. Conversely, if an Investor borrows from a New Zealand bank to buy US property, they should carefully assess risk and the cost of servicing debt for each point movement in the exchange rate.

Go here for more about the risks of investing in property and understanding the US market.